The treatment of climate risk at financial institutions has changed significantly over the past decade. Whereas it used to be viewed mostly as a reputational risk that could be addressed through the ESG agenda, climate change is now seen by many firms as a financial risk that needs to be integrated into existing risk management frameworks. This shift can be at least partially attributed to increasing regulatory attention. By providing loans to companies and direct and indirect investments, the financial industry will be exposed to firms that need to adapt to climate change. In this essay, we will assess the financial impact of climate change and discuss a risk management approach.

Climate change will affect nearly all economic sectors, but the level of exposure and the impact of climate-related risks differ by sector, industry, geography and organization. The financial impact on an organization is driven by its strategic and risk management decisions and impacts the income statement, cash flows and balance sheet.

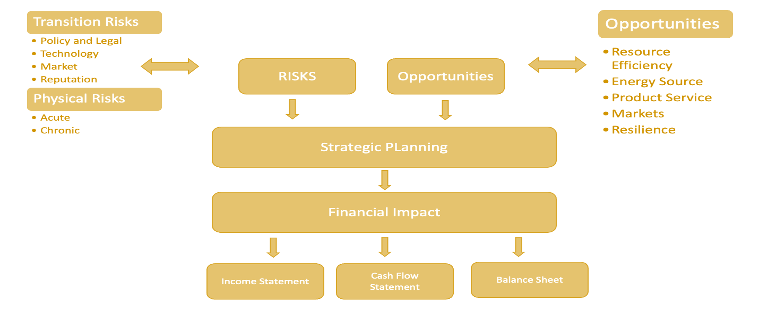

The Task Force on Climate-Related Financial Disclosures (TCFD) has developed a framework for companies to disclose their climate-related risks and opportunities. The TCFD's, although voluntary, recommendations are widely recognized as the gold standard for climate-related financial disclosures. The TCFD divided climate-related risks into two major categories, which are transition risks and physical risks.

Transition risks are the potential financial risks associated with the shift to a low-carbon economy. These risks can arise from a variety of factors, including:

- Policy risks: Changes in government policy, such as the introduction of carbon pricing or renewable energy mandates, can have a significant impact on companies that are heavily reliant on fossil fuels.

- Technology risks: The development of new low-carbon technologies can disrupt existing business models and make some companies obsolete.

- Market risks: Changes in consumer demand and investor preferences can drive down the value of companies that are perceived to be exposed to transition risks.

- Reputational risks: Stigmatization of sectors and increased stakeholder concern.

Physical risks are the potential financial risks associated with the physical impacts of climate change; they can be divided into:

- Acute: Extreme weather events, such as hurricanes, floods, and droughts, can damage property, disrupt supply chains, and cause business interruptions.

- Chronic: Rising sea levels could flood coastal properties and infrastructure, causing asset damage and business disruption.

Changes in temperature and precipitation can affect agricultural productivity, water availability and human health, all of which can have financial consequences for businesses.

Opportunities

The Task Force on Climate-Related Financial Disclosures (TCFD) recognizes that climate change presents not only risks but also opportunities for businesses and divided the opportunities in five categories, namely;

- Resource efficiency: e.g., use of more efficient transport, recycling.

- Energy Source: new technologies, lower emission sources of energy.

- Products and Services: improved brand loyalty, companies can improve brand loyalty by developing and selling products and services that are seen as being environmentally friendly.

- Markets: access to new markets, diversifying assets.

- Resilience: participation in renewable energy.

These opportunities will have a positive impact financially, operationally and on the reputation of the organization. The graph below summarizes all the risks and opportunities.

Prudential Regulation Authority

In the UK the Prudential Regulation Authority (PRA) is responsible for ensuring that the financial institutions are able to manage the financial risks posed by climate change. In 2019, it established the Climate Financial Risk Forum, which aims to address these risks. The PRA became the first regulator in the world to publish supervisory expectations that explain how banks and insurance companies need to develop an enhanced approach to managing financial risks derived from climate change. The four main areas are:

- Governance: a firm’s board should understand and assess the financial risks from climate change and have a Risk Appetite Statement including risk exposures and limits.

- Risk Management: firms should identify, measure, monitor, manage and report on the financial climate risks.

- Scenario Analysis: to analyze the business model and explore the resilience and vulnerabilities to a range of outcomes.

- Disclosure: insightful and transparent as possible, reflecting the firms understanding of the financial risks from climate change.

The PRA intends to embed the measurement and monitoring of these expectations into its existing supervisory framework.

Credit Risk and Stranded Assets

Climate change and the transition to a low-carbon economy to mitigate climate risks have significant economic costs. These costs are ultimately borne by households and firms, affecting their cash flows and wealth, which are key determinants of their credit worthiness and thus a source of credit risk. If the costs are underestimated, this will lead to financial losses and the holding assets of inadequate credit quality.

Assessing climate risks requires methodologies based on forward-looking scenarios, complex cause-and-effect linkages and data that has not been observed in the past. Even central banks need to incorporate these climate risks into their daily operations when providing liquidity to financial markets with low-risk assets as collateral.

Three dimensions play a key role in determining credit risk: a borrower’s capacity to generate enough income to service and repay the debt, as well as the capital and collateral that back the loan. The first dimension depends on a borrower’s cash flow, the second on its financial wealth and the third on the value of the collateral. Climate risks affect all three dimensions and lead to both a higher probability of default and a higher loss given defaults.

Another important credit risk is stranded assets. These assets pose a significant threat to financial markets because of their associated credit risk and potential economic impact. Stranded assets are investments that have become obsolete or have lost value prematurely due to factors such as technological advances, regulatory changes or changes in market preferences. This phenomenon is particularly important in industries that rely on fossil fuels as the world transitions to clean energy.

Fossil fuel assets are at risk of becoming obsolete due to growing environmental concerns and strict emissions regulations, and investors may find their holdings depreciating in value. This depreciation not only threatens the financial health of businesses but also increases credit risk across the financial system. Lenders in industries vulnerable to stranded assets may experience an increase in defaults and non-performing loans as the profitability of these assets declines.

Summary

Climate risk has evolved from a reputational concern to a recognized financial threat for institutions, prompting a shift in risk management approaches. The Task Force on Climate-Related Financial Disclosures identifies transition risks, linked to the move toward a low-carbon economy, and physical risks, stemming from climate change impacts. Recognizing both risks and opportunities, institutions are encouraged to disclose and manage climate-related factors. The Prudential Regulation Authority establishes supervisory expectations for governance, risk management, scenario analysis, and disclosure. Integrated risk management strategies are crucial, as climate risks affect income, wealth, and collateral, contributing to heightened credit risk and the potential for stranded assets.

Lees de volledige serie artikelen:

1. BASEL IV: A game changer?

2. Risk-Weighted Assets: Levelling the playing field?

3. Basel IV and Clearing: A clearer picture

4. Basel IV and Securities Financing Transactions (SFT)

5. Cleared Repo: A clearer view on Repos?

6. CCP: Insights of a Master Machine

7. The Euro System Collateral Management System

8. Climate Risk, the facts and the trends

9. How to Risk Manage Climate Risk: Looking for a Crystal ball

10. XVA: X-Value Adjustment