In the landscape of financial markets, instruments and strategies that enhance liquidity and efficiency are essential for maintaining stability and facilitating smooth transactions. One such strategy that plays a significant role is repurchase agreements (repo).Repos offers participants a means to optimize the utilization of collateral, enhance liquidity, and foster more efficient capital allocation. In 2008 to 2015, there has been a shift from bilateral repos to cleared repos. However, after the QE of the ECB resulting in excess liquidity cleared repos and especially general pooling became less interesting. In recent times there have been signs of recovering volumes. The question can then be asked: Are cleared repos the new normal going forward? We will discuss the differences between both bilateral and cleared repo and then go into more detail about cleared repos. Also, we will touch upon the differences between LCH and Eurex as an example of two providers of cleared repos in the EU region.

Bilateral vs Cleared Repo

A repurchase agreement, commonly known as a repo, is a financial transaction in which one party (the seller) sells a security to another party (the buyer) with an agreement to repurchase the same security at a later date and at a predetermined price. This essentially functions as a collateralized loan. The security acts as collateral and a fee or interest are paid by the seller.

A cleared repo takes this concept a step further by involving a clearinghouse. A clearinghouse acts as an intermediary between the buyer and the seller, providing a layer of risk management and ensuring the smooth execution of the transaction. The clearinghouse becomes the counterparty to both parties, guaranteeing the trade's settlement. This arrangement enhances transparency and standardisation, reduces counterparty risk, induces risk management and facilitates efficient capital allocation.

One can make a distinction between repos based on specific collateral (mostly referred to as “specials”) and General Collateral pooling/eligibility baskets.

Repos based on specific collateral are mostly called “specials”. Parties involved trade a specific asset in which the fee is a result of the “specialness” of the asset. This market segment is highly illiquid.

General Collateral pooling is a mechanism that enables market participants to aggregate a diverse range of securities into a single pool, creating a shared inventory of collateral. This pool serves as a repository from which participants can draw collateral for various transactions. Unlike specific securities, general collateral refers to a category of securities that are considered interchangeable due to their similar characteristics, maturities, and credit quality. In general, this involves triparty collateral management.

Cleared Repos

Cleared repo offers a number of advantages over traditional bilateral repo, including:

- Reduced counterparty risk: The CCP's guarantee eliminates the risk of default by one of the parties to the transaction. The Default Waterfall lines of defence ensure loss coverage in normal and extreme market conditions. In the next article we will elaborate more on CCPs and their risks.

- Increased liquidity: Cleared repo markets are typically more liquid than bilateral repo markets, as there is a greater number of participants, standardization and a wider range of collateral available.

- Reduced operational risk: The CCP absorbs the challenges of the settlement process of the transactions, which reduces the operational risk for the participants. Also, there is more standarization which helps with the operational burden.

- Reduced regulatory burden: CCPs are subject to strict regulatory requirements, which can help to reduce the regulatory burden for their participants.

- Standardization, transparency and risk management framework for all market participants

- Preferential treatment in Basel IV regarding cost of capital and more netting possibility to have less of a negative impact on the leverage ratio.

The clearing of OTC derivatives has been pushed to mandatory, while the clearing of repos is more incentivised through Basel IV capita rules.

Cleared repos, as a mechanism for secured lending, aligns with Basel IV's focus on sound risk management. The clearinghouse's role in mitigating counterparty risk aligns with Basel IV's emphasis on capital adequacy to absorb unexpected losses. By providing a centralized clearing mechanism and managing collateral, cleared repos contribute to the reduction of systemic risks and enhance transparency in the market.

While cleared repos offer numerous benefits, they are not without challenges. The potential for systemic risk still exists, as the interconnectedness of financial institutions can lead to a chain reaction of defaults in the event of a major disruption. Regulatory oversight is crucial to ensuring that clearinghouses are adequately capitalized, have effective risk management measures in place, and are well-prepared to manage stressed market conditions. Due to a lack of triparty managers, there is also potential concentration risk for market participants to be addressed in the future.

Eurex versus LCH: a product comparison

In financial markets, clearinghouses play a pivotal role in ensuring the stability and integrity of transactions. Two prominent clearinghouses, Eurex Clearing and LCH, stand out as key players in the EU financial infrastructure. While both entities share the core mission of risk mitigation and efficient settlement, they exhibit distinct characteristics that cater to diverse market needs. Below we discuss the product offerings of general collateral (GC) pooling from both.

Eurex

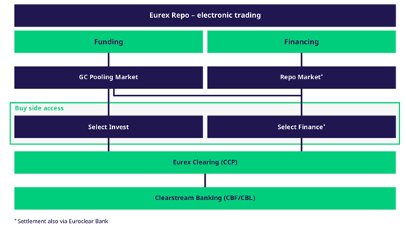

Eurex Clearing (part of Deutsche BorseGroup) has several access models available that enable clients (sell-side and buy-side) of banks to access the clearinghouse directly. While some of these models require banks to continue to participate as clearing agents (with ensuing obligations such as default fund contributions, bidding obligations and indemnities), the potential balance sheet relief is substantial (impact on cost of capital, leverage ratio). With balance sheet relief and the associated capital efficiencies, banking institutions create capacity for expanded business. Eurex offers the following products:

Full Clearing Membership

- GC Pooling: The main stream general collateral (GC) repo offering. It’s a platform where mainly banks (sell side) anonymously trade in GC baskets and are cleared by Eurex. It requires a full membership as a GCM or DCM.

Market access to trading without full clearing membership

- Select Invest: clients can act as net cash providers to banks quickly and easily, benefiting from the advantages of trading through a clearing house. It requires an ISA Direct Light Licence Holder and is designed for pension funds, corporates, insurers and money market funds.

- Select Finance: provide access to secured funding (GC Pooling) and securities financing (Repo and SecLend Market) in one single trading and clearing permission. Select Finance clients will have direct access to Eurex Clearing and will need to fulfil all admission requirements. This can be achieved by signing an ISA direct agreement with a clearing agent who will provide transaction, cash and collateral management services and fulfil default fund and bidding obligations. Examples of clients are pension funds, asset managers and insurance firms.

- Direct Market Access: means an arrangement where a member or participant or client of a trading venue permits a person to use its trading code so the person can electronically transmit orders relating to a financial instrument directly to the trading venue and includes arrangements that involve the use by a person of the infrastructure of the member or participant or client, or any connecting system provided by the member or participant or client, to transmit the orders (direct market access). So, there’s no requirement for a clearing licence and allows only trading via a clearing broker.

Eurex uses clearstream banking for custody, settlements and triparty collateral management. It is possible to fund or finance in the main currencies like USD/EUR/GBP with maturities ranging from O/N up to 2 years. The main GC basket is based on the eligible asset database by the ECB and covers approx. 3,000 eligible securities all of which fulfil the LCR HQLA Level 1 criteria. There’s an interface between euroclear and clearstream available to enhance collateral management.

Eurex uses clearstream banking for custody, settlements and triparty collateral management. It is possible to fund or finance in the main currencies like USD/EUR/GBP with maturities ranging from O/N up to 2 years. The main GC basket is based on the eligible asset database by the ECB and covers approx. 3,000 eligible securities all of which fulfil the LCR HQLA Level 1 criteria. There’s an interface between euroclear and clearstream available to enhance collateral management.

LCH

€GCPlus, a central clearing service for the triparty repo market, is offered by LCH. Clearnet SA in collaboration with Euroclear and Banque de France. Cash lenders or borrowers transact anonymously via leading electronic platforms such as BrokerTec (CME group), MTS or tpREPO among others. Any trades that are matched are then sent to LCH SA for registration and clearing. Euroclear allocates collateral for timely and accurate delivery versus payment.

It’s similar to GC Pooling in the way it works. The main basket is LCR level 1 and the maturity range is O/N up to 2 years.

In the next article we will dive deeper into the CCPs details and look at the risks and benefits of using a CCP for not only cleared repo but clearing in general.

The growth of cleared repo

The use of cleared repo has grown significantly in recent years. This is due to a number of factors, including:

- Increased regulatory requirements: Regulators have been increasingly mandating the use of cleared repo for certain types of transactions.

- Increased demand for liquidity: The growth of the repo market has been driven by the increasing demand for liquidity by financial institutions.

- Improved efficiency: Cleared repo has been shown to be more efficient than bilateral repo, which has led to its increased use.

Increased standardization and transparency.

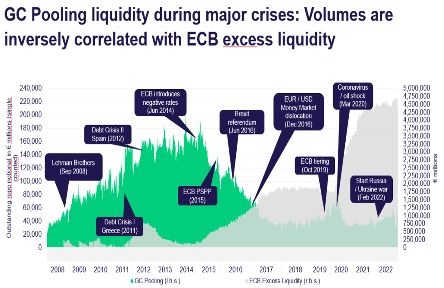

However, the most important factor regarding cleared repo volume is the inverse correlation with ECB excess liquidity as shown below.

* Graph: Eurex

* Graph: Eurex

With the normalisation of interest rates and Quantitative Tightening (QT) by the ECB, excess liquidity will diminish and will thus have a positive effect on the volume of cleared repos.

Normally, in the past EONIA was trading above the ECB deposit facility rate. Hence, it made sense for banks to give cash at a higher price via GC repos and receive collateral. QE equalized the rates, so there was no incentive anymore for banks to finance collateral. At the moment ESTR (replaced EONIA) is trading at 3,65 with ECB deposit facility at 3.75%. So, it is still more lucrative for banks to stall excess money at the ECB.

For pension funds, insurance firms, corporates and asset managers using cleared repo is a cost-effective way to finance their margin calls or working capital. More volume would probably spark more participants. Normalisation of ESTR by QT of the ECB and the favourable treatment of the cost of capital and netting possibilities will have a positive impact on cleared repo. This will also lead to more illiquidity in the bilateral repo market which has a reinforcing effect. Therefore, cleared repo is likely to become more widely used by non-financial institutions, such as pension funds and insurance companies.

Conclusion

In the dynamic landscape of financial markets, strategies that optimize collateral utilization, enhance liquidity, and promote efficient capital allocation are essential for maintaining stability and functionality. General Collateral pooling stands as a compelling solution that achieves these objectives by creating a shared repository of interchangeable collateral. By simplifying the process of accessing collateral, enhancing risk management, and offering flexibility to market participants, cleared repo plays a pivotal role in shaping the modern financial ecosystem. As markets continue to evolve, cleared repo is likely to be a crucial tool that empowers participants to navigate the complexities of collateral management and secure their financial transactions with greater efficiency and confidence.

Lees de volledige serie artikelen:

1. BASEL IV: A game changer?

2. Risk-Weighted Assets: Levelling the playing field?

3. Basel IV and Clearing: A clearer picture

4. Basel IV and Securities Financing Transactions (SFT)

5. Cleared Repo: A clearer view on Repos?

6. CCP: Insights of a Master Machine

7. The Euro System Collateral Management System

8. Climate Risk, the facts and the trends

9. How to Risk Manage Climate Risk: Looking for a Crystal ball

10. XVA: X-Value Adjustment